Benefits

Benefits

Significant reduction in false positives resulting in material savings on compliance costs

Data agnostic allowing you the flexibility to choose datasets including Dow Jones, World-Check or Lexis Nexis

Evidence risk-based overnight screening to regulators

Accelerate risk-based handling of potential matches

Materially improve risk governance via real time reporting of match handling

Self-service data quality assessment tool

World-class sanctions, PEP & watch list data sets

Unique 3D risk-based approach

Ultra-secure on-prem, web and API options

Live Adverse Media Monitoring option

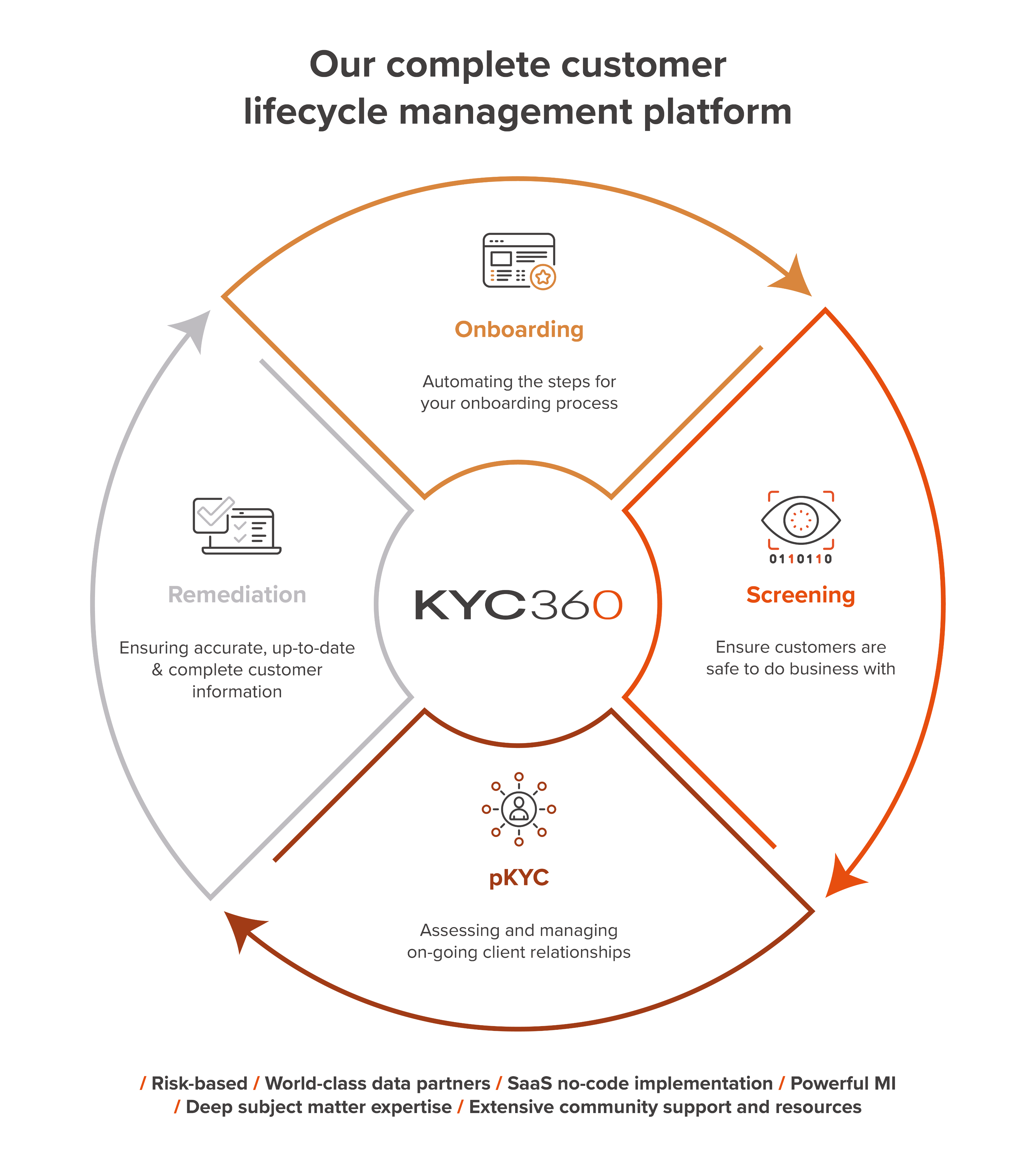

Screening is part of our complete Customer Lifecycle Management platform

KYC360’s suite of Client Lifecycle Management software solutions is designed to transform your business processes enabling you to outperform commercially through operational efficiency gains and superior CX whilst remaining fully compliant with evolving regulatory standards.